New Business Return Filing Due Dates and Penalty Changes on the Horizon

The Fourth of July has come and gone and for many business owners the mid-summer season is an excellent time to start to look ahead and begin making decisions in preparation of the end of the tax year. Part of this process should include a review of how any recent legislation may impact the business. Many such tax code changes are passed and signed into law during this time and can be overlooked when included in seemingly unrelated legislation.

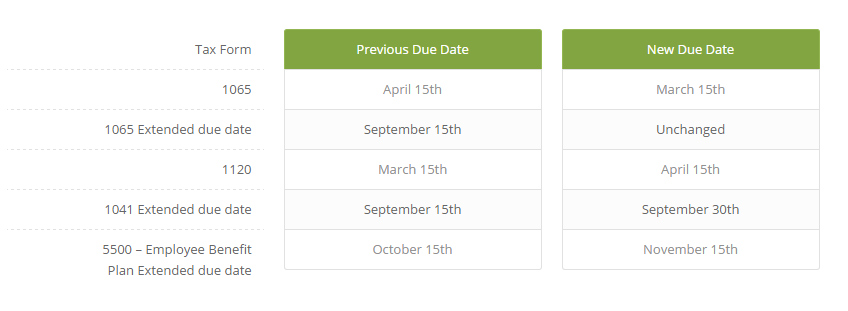

One of these such changes, The Surface Transportation and Veteran’s Health Care Choice Improvement Act of 2015, passed last summer and contained many changes to the filing due dates of many business tax return filings. The estate and fiduciary returns, Employee benefit plan returns, and report of foreign account returns are also impacted by the changes. These changes go into effect for 2016 tax returns and will impact the due dates for the upcoming 2017 filing season. The changes are as follows:

Late arrival of Schedules K-1 from partnership returns has created the need for many individuals to file a personal tax return extension. The change in the Form 1065 filing date is expected to help alleviate this need by pushing the due date back by one full month. Both flow through entities, Partnerships and S Corporations, are now due on March 15th. The extended due date remains unchanged for both Forms 1065 and 1120S. C Corporations filing Form 1120 now have until April 15th to file as they do not impact the filing of individual tax returns. These changes should help to relieve some filing season stress for both taxpayers and tax professionals alike.

The bill also included changes to a few other return filings as listed above. Fiduciary returns, Form 1041, now have an additional 2 weeks of extension time and Form 5500 now has an additional month of extension period. The foreign account reporting returns formally due in June are now due with the filing of the individual return and can now be extended for 6 months along with the Form 1040.

The Trade Preferences Extension Act of 2015, also passed last summer, included updates to penalties related to filing Forms 1099. The act increased the penalty for filing a late or incorrect form from $30 per form to $50 per form if the error or omission is corrected within 30 days of the due date and doubled the maximum penalty to $500 for intentional disregard. The penalty for 1099 forms more than 30 days late increased to $100 per form and for those corrected after August 1st to $250. For late and incorrect filings of form W-2 the penalties range from $50 to $260 per W-2 and can even mount to $530 per W-2 for intentional disregard. Timely filing of these forms is essential to avoid these penalties. It should be noted that 2016 forms W-2 as well as form 1099’s reporting non-employee compensation (box 7) need to be filed by January 31, 2017 even if they are electronically filed. This is an earlier filing deadline than in previous years. The IRS has also ramped up its efforts to encourage businesses to comply with their form 1099 filing requirements in order to lessen the occurrence of under-reporting and help close the “tax-gap” which is the difference between what is owed in taxes and what is actually reported by taxpayers.

If you have any questions regarding how these changes may impact you or your business it is recommended you contact your trusted financial and tax advisors about your individual situation.

Michelle is a Staff Accountant at Gamwell, Caputo, Kelsch & Co., PLLC in Conway, NH and can be reached at 603-447-3356. Michelle welcomes any article feedback or questions for future article consideration.